Commercial Solar Financing: PPA vs Loan vs Lease — Which One Screws You?

Australian businesses are being sold solar finance packages the way used cars get sold, with enthusiasm, speed, and critical details buried on page 14 of the contract.

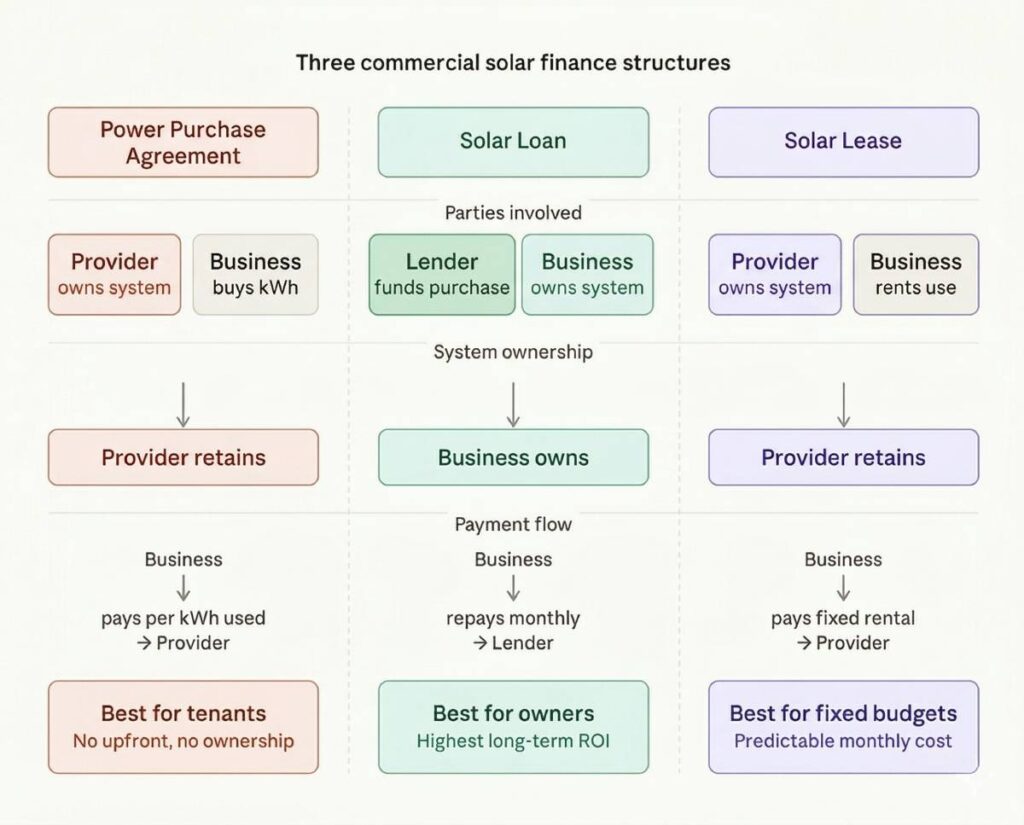

The three main structures, Power Purchase Agreement (PPA), solar loan, and solar lease, look similar from the outside but deliver wildly different financial outcomes depending on your situation. Get the wrong one, and you’re locked into a decade-long commitment that undercuts every dollar you thought you were saving.

This guide cuts through the sales pitch and shows you exactly how each option works, who it suits, and what the hidden costs actually are.

How Commercial Solar Financing Actually Works

Before comparing structures, understand the core mechanic: someone pays for the solar system, and someone profits from the energy it generates. The finance structure determines which party is which.

With a loan, you are the buyer. You own the asset from day one (or after the loan term). With a PPA or lease, a third party owns the panels on your roof and sells you either the energy (PPA) or the equipment (lease). That distinction controls your tax position, your exit options, and your long-term ROI.

Power Purchase Agreement (PPA): Zero Upfront, Zero Ownership

What It Is

A PPA means a solar finance provider installs panels on your roof at no cost. You pay them a rate per kilowatt-hour (kWh) for the electricity those panels generate, typically below your current grid rate. The provider owns the system for the duration of the contract, usually 10 to 25 years.

Where It Gets Expensive

Escalation clauses

Most Australian commercial PPAs include an annual rate escalator of 1% to 3.5% per year. Sign a 20-year PPA at $0.10/kWh with a 3% annual increase, and you’re paying $0.175/kWh in year 20, potentially above retail grid rates by that point.

Contract end scenarios

When the term expires, you typically face three options: extend the agreement, buy the system at residual value (often inflated), or have the provider remove the panels. Removal clauses can include make-good provisions requiring you to restore the roof to its original condition at your cost.

Who a PPA Actually Suits

A PPA is rational for one type of business: a tenant who does not own their premises and cannot capitalise on an asset. You get lower electricity costs, zero capital outlay, and the landlord handles structural questions. For anyone else, especially a business owner who controls their property, a PPA is the most expensive way to go solar over a 15-plus-year horizon.

Solar Loan: Highest Long-Term Return, Highest Short-Term Commitment

What It Is

A solar loan funds the purchase of a system you own outright. In Australia, these come as secured business loans (against property), unsecured commercial finance, or green energy loans from specialist lenders. Loan terms typically run 5 to 10 years, with system ownership and all financial benefits going to you.

The Real Numbers

According to the Clean Energy Council’s 2024 Commercial Solar Report, a 100kW commercial system in Australia has an average installed cost of $90,000 to $130,000. Financed over 7 years at a 7.5% interest rate, monthly repayments sit around $1,400 to $2,000, still below what most businesses pay monthly on an equivalent electricity bill.

The kicker: after the loan is repaid, your electricity from that system costs you near zero for the remaining 15 to 20 years of panel life. A PPA never reaches that point.

Tax Treatment

Under Australian tax law, owning a commercial solar system makes you eligible for:

- Instant Asset Write-Off (subject to ATO thresholds current at time of purchase)

- Depreciation deductions over the effective life of the asset

- Small Business Energy Incentive (where applicable under current legislation)

A PPA or lease gives you none of these. Your only deduction is the ongoing lease or PPA payment as an operating expense, which is deductible, but not front-loaded the way depreciation is.

Real-World Scenario

Solar Fit Solutions in Sydney typically quotes 100kW to 200kW system packages for mid-size commercial premises — the size range where a loan structure consistently outperforms a PPA over a 15-year horizon.

A Brisbane-based manufacturing facility with a $180,000/year electricity bill finances a 200kW solar system for $210,000 over 7 years. Annual loan repayments: approximately $38,000. Annual electricity savings: $68,000 (based on 60% self-consumption offset). Net annual saving during loan period: $30,000. From year 8 onward: $68,000 per year in savings with no ongoing finance cost. Over 20 years, the net financial benefit has exceeded $1.1 million.

Businesses adding battery storage to a loan-financed system should also factor in battery storage chemistry and cycle life when calculating total asset value — a quality LFP system can deliver 3,500 or more cycles before meaningful capacity degradation, which changes how you model depreciation.

Where It Falls Apart

A solar loan demands a deposit (typically 10% to 20%) and requires the business to have sufficient serviceability for lender approval. For businesses with constrained cash flow or high existing debt, the serviceability test rules this out. It is also the wrong structure for a tenant — you’re financing an asset you’ll leave behind when you move.

Solar Lease: The Middle Ground That Often Satisfies Nobody

What It Is

Under a solar lease, a finance provider owns the system, and you pay a fixed monthly rental for access to it. Unlike a PPA, the lease payment is fixed per period, not per kWh generated. You pay the same amount whether the panels produce well or poorly.

The Performance Risk Problem

This is the structure’s critical flaw. In a PPA, you only pay for what the system produces. In a lease, you pay regardless. A cloudy winter quarter in Melbourne still results in the same monthly invoice. Underperforming systems due to shading, soiling, or inverter faults don’t reduce your lease liability.

Some leases include a buyout option at the end of the term at a predetermined residual value. If that residual is set below market value, it can work in your favour. If it reflects “fair market value” which the provider defines, you can end up paying twice for the same asset.

Who are Lease Suits

A lease makes sense for businesses that need predictable monthly costs above all else — think franchises, medical practices, or any entity where budget certainty matters more than total cost optimisation. It works best on shorter terms (5 to 7 years) where residual values are cleaner and the system hasn’t aged past peak output.

Direct Comparison: PPA vs Loan vs Lease

| Factor | PPA | Solar Loan | Solar Lease |

| Upfront Cost | $0 | Deposit (10-20%) | $0 |

| System Ownership | Provider | You | Provider |

| Payment Type | Per kWh used | Monthly repayment | Fixed monthly rental |

| Performance Risk | Provider | You (insured) | You |

| Tax Benefits | Opex deduction only | Depreciation + write-off | Opex deduction only |

| Contract Length | 10-25 years | 5-10 years | 3-10 years |

| Best Exit Option | Poor (make-good clauses) | Full ownership at term end | Buyout or return |

| Best For | Tenants, risk-averse | Property owners, long-term ROI | Fixed-budget operators |

| 20-Year Total Cost | Highest (escalation) | Lowest (post-loan period) | Mid-range |

What Contract Clauses to Audit Before You Sign Anything

Whatever structure you choose, have a commercial lawyer or independent energy consultant review these specific clauses before execution:

In a PPA:

- Annual escalation rate and its cap (or lack of one)

- Early termination fee structure (commonly 80-100% of remaining payments)

- End-of-term system removal and make-good obligations

- What happens if the provider goes insolvent

In a loan:

- Redraw or early repayment penalties

- Whether the lender registers a charge over the system or broader assets

- Insurance obligations and what happens to the loan if the system is destroyed

In a lease:

- Residual value methodology fixed dollar or “fair market value”

- Who bears maintenance and inverter replacement costs

- Sub-lease restrictions (relevant if you may sublease your premises)

The Ownership Principle That Simplifies the Decision

Strip away the marketing, and one principle applies to almost every situation: if you own the property and plan to stay for 10 or more years, a solar loan produces the best financial outcome reliably, materially, and without ambiguity.

PPAs and leases exist to serve a legitimate need for businesses that cannot or will not deploy capital. They are not inherently predatory. But they are frequently mis-sold to business owners who would be better served by a loan, because the finance provider earns ongoing revenue from a PPA or lease that they do not earn from a loan.

Know that conflict of interest going in.

Key Takeaways

- PPA: Zero cost to enter, highest long-term cost if you own your property — escalation clauses are the mechanism that makes this true.

- Solar Loan: Highest short-term commitment, lowest total 20-year cost, and the only structure that delivers full tax benefits to the business owner.

- Solar Lease: Predictable costs, but performance risk sits with you — read the residual value clause before anything else.

Discussion question for the comments: Has your business been quoted a commercial solar PPA with an escalation clause above 2%? What rate were you offered, and did the provider volunteer that information upfront, or did you have to ask?

Commercial Solar Financing: PPA vs Loan vs Lease — Which One Screws You?

What Battery Is Used in Solar Systems? A No-Nonsense Guide

What Are Tree Reductions? What Are the Benefits of Tree Reduction?

Can You Transport Your Yacht Interstate Yourself?

Commercial Solar Financing: PPA vs Loan vs Lease — Which One Screws You?

What Battery Is Used in Solar Systems? A No-Nonsense Guide

What Are Tree Reductions? What Are the Benefits of Tree Reduction?